Why YIMBYs Should Support BAHFA

Guest article by Derek Sagehorn on why YIMBYs should support the Bay Area Housing Finance Authority.

Disclaimer: This guest article was written by BAHFA advocate Derek Sagehorn. I thought it was great and decided to publish itr. I’ve already heard grumblings about the upcoming $20 billion low income housing bond measure being put up amid tax fatigue. I’ve long been a supporter of BAHFA from its early stages and now. Its a rare oppertunity to make job-heavy parts of the West Bay and Silicon Valley to help fix the affordability and homeless crisis they thrusted upon the East Bay. Moreover, it’ll create low income housing in wealthy neighborhoods that have long shut them out throughout the Bay Area.

So without further ado, here’s Sagehorn:

—

On June 26th the Bay Area Housing Finance Agency (BAHFA) placed a $20bn low-income housing bond on the ballot for the 9 counties of the Bay Area. The Bay Area Housing for All (BAHA) bond would be a massive shift in the scale and administration of subsidized housing in the Bay Area. You can read arguments for BAHA for environmentalists, transit advocates, housers, tenant advocates, and service providers. I am going to focus on why YIMBYs should support BAHA.

Quick background: BAHFA as an agency is the brainchild of long-term Bay Area housers Heather Hood and Geeta Rao from Enterprise Community Partners. They published a white paper in 2018 called “The Elephant in the Region” which called for a regional housing finance agency housed within the Metropolitan Transportation Commission (MTC) to overcome the balkanization of housing finance in a region of 101 local governments, the thin-to-non-existent public sector capacity and lack of scale to address the depth of need. That white paper turned into legislation via AB 1487 (authored by then Assemblymember and current SF City Attorney David Chiu) to create the Bay Housing Finance Agency. AB 1487 was attacked by the Right NIMBYs of Livable California and Left NIMBYs of 48 Hills but was eventually signed into law by Gov. Newsom.

Once passed MTC got to work standing up BAHFA. The first thing they did was hire Kate Hartley, a former housing chief for San Francisco with decades of experience financing and building subsidized housing. Over the past four years BAHFA identified housing needs, conducted outreach, researched revenue measure options and developed a draft business plan. Based on this work BAHFA proposes that a $20bn BAHA bond be used to 1) underwrite county-level subsidized housing efforts and protections based on expenditure plans approved by BAHFA with 80% of revenue returning to source; 2) use the 20% regional share to fund a BAHFA Business Plan focused on delivering and preserving low-income housing quickly and efficiently in terms of cost; and 3) providing tenant protections in the form of rent supports for those at-risk of homelessness and eviction counsel.

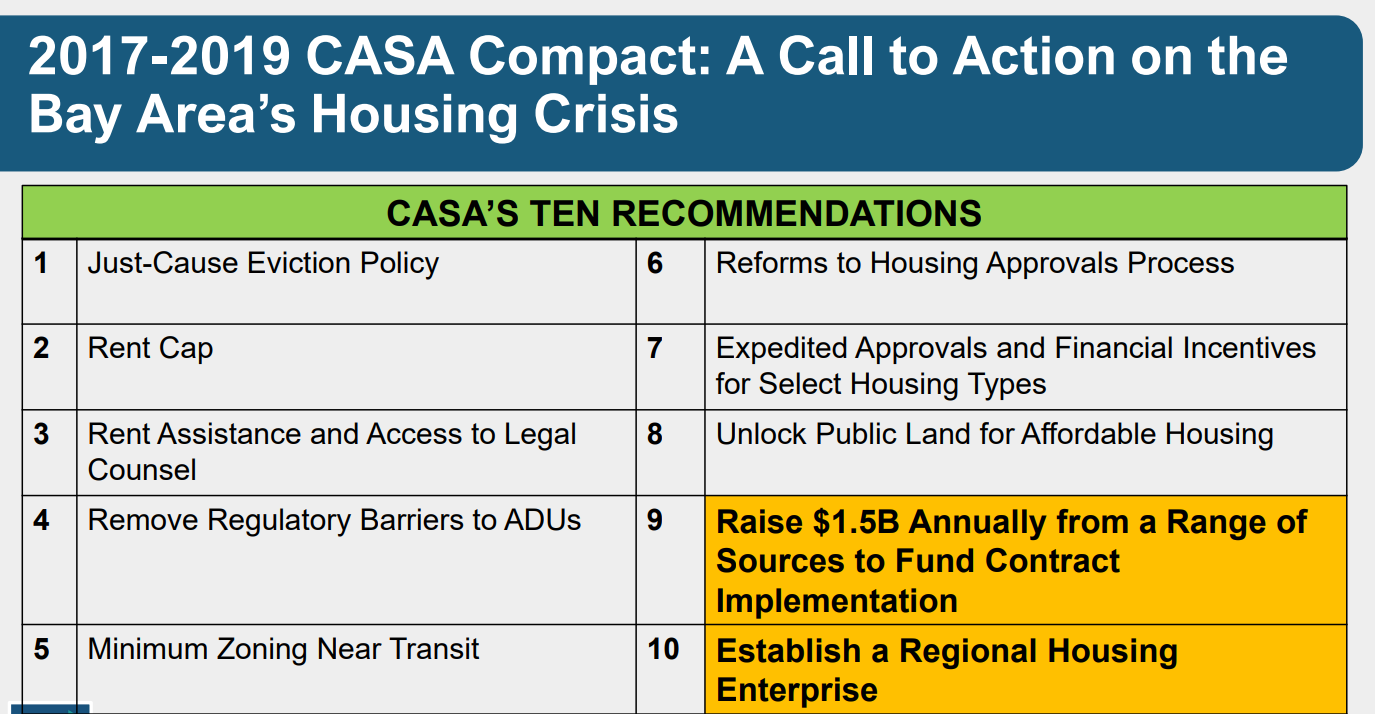

If this sounds familiar it’s because the focus on Production, Preservation and Protections, or the 3 P’s for housing, were generated as part of CASA Process put on by MTC between 2017-2019 to get regional consensus. The whole housing sector, from construction labor, developers, landlords, tenant advocates, housers, local governments, planners and equity nonprofits sat down over two years and tried to get consensus for reforms to address the Bay Area’s decades-long housing crisis. A regional housing finance agency ended up on the list of recommendations for the CASA Compact along with ending single family zoning, by-right approvals, upzoning transit areas, rent caps and just cause eviction protections.

Now I get that some people may look at another bond with a jaundiced eye. They’ve seen local bonds for subsidized housing get mired in ineffective administration, NIMBYism and high construction costs. The oft quoted specter of newly constructed low-income housing that costs $1m per unit is a real challenge for both the industry and housing affordability in the Bay Area. What’s different this time? Why should voters tax property owners for this?

Here are four reasons:

Housing Affordability

The primary reason YIMBYs should support the bond is that there are tremendous housing needs for low-income groups. 1.4 million people in the Bay Area spend more than half of their income on rent. The Regional Housing Needs Assessments for the Bay Area identifies that 180,000 homes affordable to low-income households are needed.

While giving low-income people cash or expanding Section 8 Housing Choice Vouchers may be preferred for a variety of reasons, it is unclear whether the political will exists at the Federal level to do either of those things. In the absence of Federal action it is up to the region to act to produce these homes. Direct subsidies for construction of subsidized housing are also sorely needed to support rental housing options in high-resource areas (places with good schools and jobs) where there aren’t rental options or private landlords discriminate against Section 8 voucher holders.

In addition, thanks to YIMBY laws like SB 35/423, Housing Accountability Act, and AB 2011 there are hundreds of entitled, ready to build low-income housing developments representing 41,000 units that just need funding. Historically subsidized housing has been subject to discretionary review or completely zoned out from NIMBY neighborhoods and suburbs so the slow speed of entitlement meant that available funding existed for nearly all approved projects. Now, with YIMBY laws in place and NIMBY veto points removed, the binding constraint on low-income housing development in California is financing. The BAHA bond and BAHFA Business Plan can unkink this production hose with financing and get shovels in the ground.

Regional Problems/Regional Scale

The Bay Area’s balkanized governance of 9 counties and 101 local governments contributes to so many problems in transit, transportation, jobs, inequality and… yes housing finance.

In 2022 Oakland passed a $850m infrastructure/housing bond. That follows on a prior infrastructure/housing bond from 2014. Oakland is a poor city with lots of housing affordability problems. The City of Piedmont, which is an extremely affluent and racially/economically segregated enclave within Oakland, has never passed an affordable housing bond to support low-income households. Piedmont is not an island. It relies on Oaklanders and others throughout the region to mow its lawns, care for its elderly, staff the hospitals, and educate its students. Moreover Piedmont benefits from the job access and infrastructure provided by the rest of the region. Like many affluent communities that have locked out renters via land use policy… the politics for Piedmont to tax itself for public goods just isn’t there.

You could repeat this exercise across the nine countries: some local governments have chosen to tax themselves (despite lower tax bases and thus higher effective rates) in order to address the low-income housing shortage while more exclusionary cities have sat on their hands. Given the intra-regional wealth and income disparities the Bay Area will never be able to get a hold on the issue without a region-wide approach.

The BAHA Bond and BAHFA Business Plan represents a chance to tap into the resources of the richest metro in the United States – no more free riders. If Piedmont cannot accomodate low-income housing then Oakland can use Piedmont’s BAHA revenue to build low-income housing in Oakland.

In addition to resource sharing between exclusionary and poorer cities the BAHA Bond and BAHFA Business Plan will provide cities that want to do the right thing (build low-income housing!) but lack the resources to properly administer a housing finance program with funding and regional public sector capacity. Rather than farming out this work to consultants or nonprofits smaller cities that want to build can tap into regional technical assistance through BAHFA.

Cost Reform

The escalation of development costs for low-income housing is a primary threat to be able to gain political support for subsidies and actually deliver homes for low-income households. If market-rate housing construction costs $300k per unit and a low-income housing unit costs $1m per unit this dysfunction is leaving extra homes on the table. Figuring out how to bend the cost curve on subsidized (and market-rate) housing is a critical mission for YIMBYs and housers alike.

The good news is that BAHFA is acutely aware of this problem, has a preliminary strategy to mitigate cost escalation and wants to get value for both low-income households and taxpayers.

Before we get into the specifics, let’s look at what the literature says on high construction costs for subsidized housing with special attention to California.

In 2020 the Terner Center published “The Costs of Affordable Housing Production: Insights from California’s 9% Low-Income Housing Tax Credit Program.” Author Caroline Reid identified several drivers of increased cost, including:

Low densities (sometimes as low as 20 units) enforced by local land use regulation and certain financing regimes do not allow for scalar efficiencies in civil works, utilities, structural elements and common space.

Discretionary approvals required by local governments increase carrying costs for projects in terms of interest, pre-development costs, and professional services. Lengthy entitlement processes require litigation contingency and push out year of expenditure for hard construction costs further increasing costs.

Structured parking and elevator costs each add between $35k and $38k per unit.

Impact fees charged by local governments for schools, parks and infrastructure have increased dramatically in response to Prop. 13 fiscal challenges.

Financial complexity for low-income housing increases the time, professional services, project scope and coordination for low-income housing. Each funder (local government bonds/trust fund, Housing and Community Development, Tax Credit Allocation Committee, California Debt Limit Allocation Committee, community development financing institutions, banks) has a preference to be the last dollar of debt/equity in order to spread risk or get their hands on many projects as possible rather than fully fund a smaller number of projects (as is the approach taken by many social housing systems). With each discrete source of financing comes additional “everything bagel” project requirements like small business participation, unit mix, LEED certification, political boycotts on suppliers/vendors from certain states/countries that drive up costs and sometimes conflict with each other. Terner found that each discrete source adds $6,400 to per unit costs with most projects having between 4-8 funding sources and some as many as 20.

It’s important to remember that this report came out in 2020. What has changed in the last four years?

Low Density Zoning: in 2022 California upzoned hundreds of thousands of parcels along commercial corridors to allow 4-8 story mixed-use housing via Asm. Buffy Wicks AB 2011.

Discretionary Approvals: in 2023 California passed Sen. Scott Wiener’s SB 423, which extended and expanded the by-right approvals and CEQA streamlining for infill housing.

Parking: in 2022 California eliminated parking minimums near transit via AB 2097.

Impact fees: in 2021 California passed AB 602 to require impact fees to be set proportionally to the size of homes (rather than number of units) thereby removing a disincentive to smaller, lower cost units and increasing transparency of fees.

The BAHFA Business Plan wants to capitalize on these YIMBY victories. Specifically the BAHFA Multifamily Rental Production Fund will be prioritizing projects that use streamlining via SB 423 or the Housing Accountability Act and reduce or eliminate off-street parking in low VMT geographies. The BAHFA Multifamily Rental Production Fund also “expects to impose per-unit caps on its lending in the interest of achieving cost control goals and shifting the industry perspective towards more cost-efficient development.”

In addition the BAHFA Innovation Fund is specifically targeted at cost control:

“The region’s affordable housing costs continue to rise at a pace that impedes the Bay Area’s ability to deliver the housing it needs. BAHFA is intent on encouraging cost control by prioritizing innovation as well as known methods for achieving cost savings (e.g., streamlined entitlements, efficient design, and reducing the number of different capital sources per development). This approach does not mean quality is sacrificed. Rather, it shifts perspective – we need more housing and, by demanding a cost-focused approach, we can bring costs down and thus more effectively deliver housing at the scale needed.”

Controlling construction costs is no easy task. It’s a thorny problem and there’s clearly more work to do for YIMBYs and housers at the state level on impact fees, single stair reform, financing coordination, elevator reform, local building codes preventing repeatable designs and prefabricated housing standardization. But the BAHFA staff are focused on trying to control costs through policy through the levers available to them.

Reforming Low-Income Housing Delivery

The existing low-income housing system is heavily reliant on the Low Income Housing Tax Credit (LIHTC) system to provide corporate and financial institution equity for nonprofit and for-profit low-income housing developers. This system is the largest and most reliable source of funding for low-income housing. It has several drawbacks, including complexity and a burgeoning professional services sector that attends to that complexity, but one stands out: the lack of public or community asset ownership means units have a limited term of affordability and subsidies cannot be recovered as equity. The siloed corporate nature of each separate development (structured as its own LLP with sponsoring bank/corporation) prevents nonprofits and public agencies from tapping into equity of existing stabilized buildings to build more low-income housing – which is standard practice in European and East Asian social housing. The fractured corporate ownership also inhibits scalar efficiencies in terms of construction, operations and financing.

In response to these challenges, BAHFA’s Innovation Fund proposes “investing in cost-effective housing that does not require low-income housing tax credits and tax-exempt bonds, which have been oversubscribed in recent years.” This means BAHFA can explore different models including cost rentals for moderate-income households, permanent supportive housing with operating subsidies and mixed-income social housing like Montgomery County.

In addition the BAHFA Business Plan proposes to create a revolving fund that provides a long-term source of capital for the region’s low-income housing developers. Once loans are recycled BAHFA can re-lend in new projects, offer debt to preserve or fix up older housing or provide rental assistance. By creating long-term regional public assets that return to source BAHFA can ensure the 2024 BAHA bond dollars continue to provide value for decades – as opposed to a one-time grant to a for-profit LIHTC developer for a limited term of affordability.

The people behind BAHFA have put a lot of thought into how the existing subsidized housing system is not working and have a credible plan to reform it to deliver sorely needed homes for low-income people. That plan relies on existing YIMBY laws and policy (and future YIMBY law and policy) but it needs YIMBY votes, door knocking and text banking for the BAHA Bond in November in order to get started.

—

This article was written by Derek Sagehorn and written by him, independently. It does not represent the positions of my employer. I do, individually, support BAHFA.

BAHFA is simply the latest in a long line of predatory legislation whose impact is to increase displacement pressures on low-income multi-generational Black homeowners. I have 2 fundamental issues with BAHFA which is why I am not supporting it. I have previously supported every parcel and property tax that came down the pike, but at some point, I must stop being complicit in the exploitation of my community, and stand up for justice and equity.

BAHFA had the choice between choosing a parcel tax or an ad valorem property tax. They choose the predatory ad valorem property tax. The difference? Parcel taxes can allow for low-income and senior citizen exemptions, while the ad valorem property tax does not. Property taxes are, therefore, predatory.

My mom is a retired school teacher with income of just over $40K/yr. She cannot currently afford her property taxes, and BAHFA - and the raft of other property/parcel taxes slated for the Novermber ballot - are increasing the pressure on her to sell her home because she cannot pay them without borrowing. Social security pays just over $36K/year. While the low-income exemption is set at the too-low amount of $35!K, she would qualify for some relief under the senior exemption. We must increase the low-income exemption and index it to CPI so that it increases in time.

My Mom lived in Oakland for 75+ years before being forced out. Is that what BAHFA is meant to do - displace our longest term, lowest income homeowners? I hope not, but that is the impact.

Given the fervor I've heard from some YIMBY's for getting rid of Prop 13, I wouldn't be surprised to hear some YIMBY's in favor of this result. Additionally, it raises real estate transfer tax and higher property taxes by reassessing her former home to market value upon sale. I know some YIMBY's, and others, support this result of forcing turnover of homes that have a low assessed value. It has been a common theme in Oakland, and elsewhere, to reduce property ownership by Black property owners in order to recapitalize our properties at higher values.

Secondly, renters must contribute to affordable housing. I have now asked a number of renters if they would contribute directly to the affordable housing trust fund. None have said they would. While there is almost universal support amongst renters for BAHFA, no one wants to make a direct contribution. Renters are a majority of Oakland's population, and must begin to directly contribute financially to mitigate the impacts of the gentrification and displacement caused by newer arrivals.

What sense does it make to tax low-income homeowners making < $50K/yr, while exempting council members with household income of $250K/yr. This is predatory, unjust, and inequitable

I implore you to reject BHAFA until 2 changes are made:

- reject BAHFA until they come back with a parcel tax rather than an ad valorem property tax

- implement a mechanism so that renters are contributing their fare share directly

My Mom thanks you.

#TaxTheRichNotThePoor

#RentersFairShareTax